![<?echo $_SERVER['SERVER_NAME'];?>](/template/twentyseventeen/skin/images/header.jpg)

The main points:

Let's try to calculate the theoretical price of the 1809 contract for Shanghai crude oil. Suppose that on March 26, the US dollar against the renminbi is 6.35, and the Oman crude oil July contract price is $65/barrel. The sum of the various costs is $2/barrel. Then the theoretical price of the SC1809 contract is (65+2)*6.35=425.45 yuan/barrel.

After estimating the theoretical price of SC1809, the opening trading strategy on the first day of trading can be formulated. If INE's listed benchmark price is significantly lower than the theoretical price, then the probability of opening price increases is large, and investors are advised to make a buy operation. Conversely, if INE publishes a listed benchmark price that is significantly higher than the theoretical price, investors can try to sell the operation. Based on historical experience and the importance attached by the exchange to crude oil futures, we expect INE's listing benchmark price to be higher than the theoretical price.

As the Shanghai International Energy Trading Center will announce the listing benchmark price on March 23, the specific time is not fixed. After the announcement of the benchmark price, the external market may still be trading. If the external disk fluctuates greatly, it will affect the opening price on March 26. By analogy, the US dollar exchange rate has a similar situation. Therefore, BOC International Futures will continue to track the closing price and real-time exchange rate of foreign crude oil futures, providing investors with the theoretical price of Shanghai crude oil futures. Investors are welcome to keep an eye on our strategy updates for the weekend.

1. Matters related to the trading of crude oil futures

1. Time to market

Crude oil futures will be listed and traded on March 26, 2018. The auction will be held at 8:55-9:00 on the same day and will open at 9:00.

2, trading time

Monday to Friday, 09:00-10:15, 10:30-11:30 and 13:30-15:00, continuous trading hours, Monday to Friday 21:00 - 02:30 the next day. No trading is allowed for consecutive trading hours on the first business day prior to the statutory holiday (excluding Saturday and Sunday).

3. Contract

SC1809, SC1810, SC1811, SC1812, SC1901, SC1902, SC1903, SC1906, SC1909, SC1912, SC2003, SC2006, SC2009, SC2012, SC2103.

4, the benchmark price

Announced by the Energy Center on the previous trading day of listing.

5. Trading margin and price limit

The trading margin exchange standard is 7% of the contract value; the price limit is 5%. The first trading day's price limit is 10% of the benchmark price. After the research, it was decided that our client's crude oil futures margin standard is 12% of the contract value.

Foreign non-brokers and foreign clients can use foreign exchange funds as security deposits. For foreign exchange funds as the margin, the central parity of the RMB exchange rate announced by the China Foreign Exchange Trading Center is used as the benchmark price for the market value. Currently, the energy center can use the foreign exchange currency as the margin as USD, with a discount rate of 0.95.

The market value of foreign exchange funds before the market closes on the day is first calculated according to the central parity of the RMB exchange rate announced on the day before the China Foreign Exchange Trading Center. At the time of daily settlement, the foreign exchange funds shall be re-determined as the base price for the use of the margin and the discounted amount shall be adjusted as described above.

6, the position announced

When a contract position reaches 200,000 lots (two-way), the Energy Center will announce the volume of the top 20 futures companies and the foreign special brokers in the month's contract, the amount of open positions, and the positions held.

Second, the benchmark price of crude oil futures

As we said earlier, the benchmark price of crude oil futures is announced on the trading day before the listing. The so-called listed benchmark price is the benchmark price of the trading before the opening of the first trading day of a new listed futures product announced by the exchange. For example, the exchange announced that the Shanghai crude oil futures 1809 contract listing price of 420 yuan / barrel, which means that before the opening of March 26, the crude oil 1809 collection bid is based on quoting 420 yuan. The general exchange will announce the listing benchmark price a few days before the new product is listed. The Shanghai crude oil futures will be announced on the trading day before the listing, which is announced on March 23, and the specific time has not been announced.

We know that the current major crude oil futures WTI and Brent crude oil are trading almost all day. After INE announced the benchmark price of Shanghai crude oil on the 23rd, the crude oil in the outer disk may still be in the transaction. If a large increase or decrease occurs, it will affect the opening price of domestic crude oil on the 26th. In other words, on March 26, investors should be long or short on the basis of the benchmark price of crude oil futures? Estimating the direction of the long and short will be extremely important for the first day of trading.

How should investors predict the direction of long and short? To make a correct judgment, we must start from the basis of Shanghai crude oil futures pricing.

Table 1: Shanghai crude oil futures deliverable oil grade, quality and premium standards

|

Source: INE, BOC International Futures

According to the deliverable oils released by INE, six of the seven oils are crude oil in the Middle East, and only one is Chinese local crude oil. China's current dependence on crude oil imports is as high as 70%, which means that most of the crude oil is imported. Among the imported crude oil, Middle East crude oil has occupied a relatively large share. Therefore, the pricing of Chinese crude oil futures is based on the Middle East crude oil price is a very logical inference. Among the six Middle Eastern crude oils, Oman crude oil is one of the deliverable oils of Shanghai crude oil futures, while Oman crude oil has futures trading, namely DME Oman crude oil futures, which is publicly traded in the market and can be physically delivered to obtain Oman crude oil. In principle, industrial customers participating in DME Oman crude oil futures trading can obtain Oman crude oil at a lower threshold. The other deliverables of Shanghai crude oil futures, such as Dubai, Abu Zakum, and Basra light crude oil, are more complicated to price, and their prices are not easy to obtain. Therefore, we can refer to Oman crude oil for the calculation of the benchmark price and opening price of Shanghai crude oil.

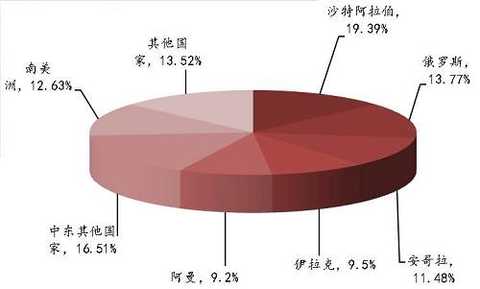

Figure 1: China's crude oil imports in 2016

|

Source: General Administration of Customs, BOC International Futures

After determining the target of the pricing calculation, another problem needs to be solved. The latest contract for the listing of Shanghai crude oil futures is 1809, which will be delivered after half a year. Considering the storage or holding costs, you need to find the corresponding Oman futures contract. In general, Oman crude oil takes about two months from shipment to warehousing, which means that the SC1809 contract needs to refer to Oman's July crude oil contract. Finally, we also need to calculate the cost of Oman crude oil shipped from the Middle East to the country, including Oman futures delivery costs, sea freight, insurance, loss, domestic delivery, storage costs.

Now let's try to calculate the theoretical price of the 1809 contract for Shanghai crude oil. Suppose that on March 26, the US dollar against the renminbi is 6.35, and the Oman crude oil July contract price is $65/barrel. The sum of the various costs is $2/barrel. Then the theoretical price of the SC1809 contract is (65+2)*6.35=425.45 yuan/barrel. In addition, we can also use the Oman crude oil active contract, which is currently calculated as the 05 contract. The obtained price plus the two-month storage fee is the theoretical price of the SC1809 contract, which will not be repeated here.

Third, the first day trading strategy of Shanghai crude oil futures

After estimating the theoretical price of SC1809, the opening trading strategy on the first day of trading can be formulated. If INE's listed benchmark price is significantly lower than the theoretical price, then the probability of opening price increases is large, and investors are advised to make a buy operation. Conversely, if INE publishes a listed benchmark price that is significantly higher than the theoretical price, investors can try to sell the operation. Based on historical experience and the importance attached by the exchange to crude oil futures, we expect INE's listing benchmark price to be higher than the theoretical price.

As the Shanghai International Energy Trading Center will announce the listing benchmark price on March 23, the specific time is not fixed. After the announcement of the benchmark price, the external market may still be trading. If the external disk fluctuates greatly, it will affect the opening price on March 26. By analogy, the US dollar exchange rate has a similar situation. Therefore, BOC International Futures will continue to track the closing price and real-time exchange rate of foreign crude oil futures, providing investors with the theoretical price of Shanghai crude oil futures. Investors are welcome to keep an eye on our strategy updates for the weekend. (Zhongyin International Futures Research Gu Jintao)

(Editor: Shao Yidi HF116)

Cable Insulation Tape,Pure White Non Woven Tape For Cable,Polyester Fabric Water Blocking Tape,Strengthened Light Weight Non Woven Fabric

Jiangsu Super Prosperous New Material Co., Ltd , https://www.jschaowang.com